What Is Fraud Prevention?

Organizations use processes, tools and strategies in order to detect, deter and mitigate fraudulent activities. This is what we call fraud prevention. Among these activities, there can be financial frauds, identity frauds and cyber-related crimes. Nowadays, proactive and data-driven approaches have become necessary in every organization’s workflow.

Why Businesses Need Fraud Prevention Activities?

Let’s start with a topic that you might have been expecting: Cybercriminals. The methods that cybercriminals use become more and more advanced each day. They may impersonate individuals through deepfakes, bypass verification processes with synthetic identities, and execute phishing scams to steal sensitive information. It is almost impossible to keep up with these methods, so fraud prevention becomes a must for businesses.

Aside from cybercriminals, there is a looming regulatory pressure that we cannot possibly overlook. Businesses must navigate numerous complex regulations. Some notable mentions are Anti-Money Laundering (AML) laws, the General Data Protection Regulation (GDPR) for data privacy, and the Payment Card Industry Data Security Standard (PCI DSS) for payment security.

In addition to these two, there are reputational implications as well. In today’s digital age, trust has become more important than anything. It only takes a single fraud incident to destroy years of carefully built relationships and the implications most likely won’t be limited to relationships because it can also cause customer churn, negative press, and long-term damage to a company's credibility.

Lastly, the financial impact of fraud is staggering. Last year, global fraud costs exceeded $500 billion and it doesn’t seem to stop anytime soon. These losses disrupt entire industtries and economies, so there is an urgent need for robust fraud prevention measures.

Why Fraud Prevention Important?

There is a non-negligible rise in cases across various industries, and this has led fraud prevention to gain vital importance. Here, we have listed several reasons.

Rising Digital Threats

There are new digital vulnerabilities like phishing attacks, deepfaked onboarding processes, and synthetic identity fraud. All of these require businesses to reinforce their fraud detection strategies.

Increased Regulatory Scrutiny

Businesses need to possess robust compliance frameworks due to regulations like AML and GDPR, and if they fail to do so, they may face all kinds of repercussions.

Reputational Risk

As we have mentioned in the previous paragraphs, the results of a fraud incident do not remain confined to monetary losses, such as damage to customer trust and long-term implications to business relationships.

Financial Losses

Fraud-induced monetary losses have never been this high before. This clearly shows how important it is to invest in advanced fraud prevention measures.

Common Trends of Fraud to Watch in 2025

Let’s touch upon payment fraud first. There are two notable examples that we can list under this type of fraud. The first one is known as credit card misuse and it is carried out by a fraudster using stolen card details to make unauthorized purchases. These types of losses exceeded $32 billion in 2022. Following the credit card misuse, we must mention the chargebacks due to unauthorized purchases. This occurs when a customer claim these as unauthorized and then disputes legitimate transactions. This costs both additional charge-back fees and the lost revenue.

Now, let’s move on to the identity fraud. Similarly to the first paragraph, we will divide this into two as well. Four years ago, creation of synthetic identity fraud costed U.S. lenders an estimated $6 billion. Fraudsters achieve this by merging real and fabricated information to create fake identities and then use these to open accounts or obtain credit. The second example is Deepfake-Based Onboarding Manipulation, where fraudsters aim to bypass biometric verification system with advanced AI tools that create realistic fake videos or audio.

Third major type of fraud is account takeover. Fraudsters use automated tools to test stolen logic credentials across multiple platforms. Another way that they execute account takeover is phishing attempts that lead to unauthorized account access. Attackers trick users into sharing their login details through fake emails or websites.

Business Email Compromise (BEC):

Fraudsters may also impersonate executives or vendors in order to trick other employees with fake invoices or fraudulent wire transfers to transfer large sums of money. This is also called Business Email Compromise and FBI’s data show that these scams caused losses of $2.7 billion globally in 2022.

The threat doesn’t always come from outside. Insider threats have become very prevalent and can encompass data theft, unauthorized system access, or financial embezzlement. 20% of organizations report at least one case of insider fraud each year.

Last but not least, we cannot skip loan or insurance fraud because it alone costs the indus-try over $80 billion annually in the U.S. Fraudsters submit fabricated loan applications or insurance claims with forged documents. The staged accidents and fake injuries are common examples in this one.

Fraud Prevention Checklist (2025 Edition)

Identity & Onboarding Controls

Government-issued ID verification (OCR + biometric match) can allow you to accurately verify every user’s identity with the help of cutting-edge optical character recognition and biometric matching technologies. In order to prevent spoofing or fraudulent attempts, you can also perform liveness detection or selfie check to confirm the presence of user during onboarding. Another thing you can carry out to minimize compliance risks is sanctions and PEP list screening during onboarding, in order to match users against global sanctions and Politically Exposed Persons (PEP) databases. Also, you can identify and prevent duplicate accounts or devices with intelligent fuzzy logic algorithms.

Behavioral & Transaction Monitoring

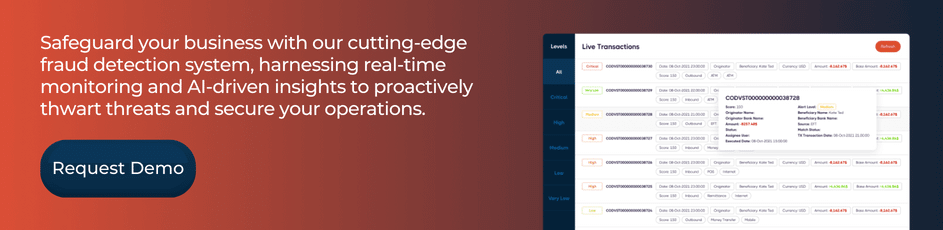

To put these into practice you must implement real-time transaction monitoring system in place. Also, you can set up rule-based alerts for suspicious patterns because there is a persisting risk of anomalies such as high transaction frequency or mismatched geographical data. The risk can depend on several factors so, custom risk scoring models applied per customer type can improve accuracy and reduce false positives. Lastly, manual review workflow for flagged activities by having expert teams to review and investigate flagged activities can be a great help.

Authentication & Access Security

Authentication and access makes a very important part of the fraud prevention. You can implement Multi-Factor Authentication (MFA) for all users, role-based access controls for internal staff, automated session timeout and IP monitoring and lastly, login anomaly detection (device, time, location) to address the possible problems on this side.

Internal Risk Controls

When it comes to internal risk controls, the first measure you can take is to segregate the duties in financial approvals. This way no single employee can have end-to-end control over financial processes. Subsequently, you may decide to conduct frequent checks to reconcile accounts and reports regularly so that all accounts and transactions are accurate and balanced. Also, on a quarterly basis, you can conduct employee fraud awareness training to educate staff on recognizing and handling fraud risks.

Reporting & Audit Trail

To pick up where we left off, STR/SAR process are another thing to train employees for. While doing so, you must also well-document suspicious transaction and activity reporting procedures. In addition to these trainings, businesses must maintain detailed records of high-risk activities for future audits and investigations. Another thing that must be done is the assignment of escalation matrix and fraud response team to define a clear escalation process and handle incidents promptly.

Post-Incident Response

You must regularly review and test the incident response plan in the past 12 months to ensure readiness for fraud incidents. Also, step on it to communicate impacted users by offering support and compensation when necessary. When a fraud case ends, you must analyze the root cause of fraud and ensure appropriate action is taken.

Best Practices for Fraud Prevention in 2025

A multi-faceted approach to fraud prevention must be preferred by organizations. We have listed the most efficient practices below.

Strengthen KYC Protocols

Your organization should apply Enhance your Know Your Customer (KYC) procedures and in order to do so, you can use advanced tools like biometric ID verification, video KYC, and document scanning. These technologies can be of great help validating customer identities during onboarding, thus it reduces the risk of fraud from the start.

Apply a Risk-Based Approach

The level of risk can vary between transactions, so taking a risk-based approach to monitoring is ideal. High-risk transactions, particularly high-value transfers or activities in regions historically associated with fraud, should be the ones you must pay close attention to.

Enforce Multi-Factor Authentication (MFA)

Multi-factor authentication (MFA) comes very handy for sensitive actions like administrative access, user logins, and high-value financial operations. With MFA users must verify their identity through multiple methods, such as a password, a security token, or a biometric factor like a fingerprint, in order to strengthen security dramatically.

Leverage AI for Automated Fraud Monitoring

It is not really difficult to come across AI in several industries, so why not take advantage of it in this case as well? AI-powered tools and machine learning algorithms can monitor transactions and detect anomalies in real time. There are unusual patterns that you may encounter such as deviations in spending habits or suspicious login attempts. With these technologies, you can identify these and flag them for review.

Educate Employees and Customers

Human error often plays a significant role in fraud incidents and education plays a critical line of defense in avoiding these. So, you had better invest in fraud awareness programs that cover topics such as phishing, social engineering, and best practices for handling sensitive data for your employees.

Create an Incident Response Plan

In fraud prevention, you must always prepare for the worst. For this reason, establish a clear incident response plan to manage fraud scenarios effectively, in which there should be the steps for suspicious activity investigation, incident reports for appropriate authorities, and neutralization of potential threats.

Leading Tools and Technologies for Fraud Detection

Here are some cutting-edge tools and their applications that you can use to combat fraud more effectively.

| Tool Type | Examples / Features |

| Transaction Monitoring | Rule-based + behavioral analytics (e.g., Sanction Scanner) |

| Identity Verification | Biometrics, liveness detection (e.g., Onfido, IDfy) |

| Device Behavioral Analysis | Device fingerprinting, tracking mouse and keystroke patterns |

| Sanctions and Blacklist Screening | Screen against sanctions, PEPs, and fraudster lists |

| Machine Learning Models | Real-time anomaly detection in large-scale datasets |

Fraud Prevention in Different Industries

In banking and fintech, you must deploy KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance systems to detect suspicious activity, which can reduce fraud cases by up to 70%. In addition to these, you should consider transaction scoring because it helps flag high-risk activities and thus, protects assets worth billions annually.

There is a prevalent type of fraud that is called chargeback fraud in e-commerce which costs merchants over $20 billion each year. You can combat this with the help of address validation tools and fraud scoring models. These are proven to improve detection accuracy by 85%.

Whereas in healthcare, monitor insurance claims and provider-generated data for inconsistencies, help the industry to save an estimated $300 billion each year.

Fraud poses a high risk for telecom as well. A notable example is SIM card swap fraud. It has increased by 400% in recent years. Suspicious identity alterations in mobile accounts are also another risk worth-mentioning. You must prevent these to enhance customer security.

Let’s finish with a more recent industry: Crypto and Web3. In order to ensure safety and transparency in these decentralized systems, you must use wallet screening mechanisms to identify fraudulent addresses and detect the misuse of smart contracts.

FAQ's Blog Post

Implementing multi-factor authentication, employee training, and real-time monitoring are among the most effective fraud prevention strategies. These reduce both internal and external threats.

Businesses can detect fraud early by using AI-powered analytics and setting up automated alerts for suspicious transactions. Early detection minimizes financial loss and reputational damage.

Well-trained employees are better equipped to recognize phishing, social engineering, and internal fraud risks. Regular training builds a culture of compliance and awareness.

Fraud prevention tools analyze patterns, flag anomalies, and block high-risk activities in real-time. They use machine learning to improve accuracy over time.

Data encryption secures sensitive information during storage and transfer, preventing unauthorized access. It’s a core component of cybersecurity and fraud prevention.

Yes, many fraud prevention tools offer scalable pricing for small businesses. Simple steps like employee awareness and basic software can significantly reduce risk.

Fraud risk assessments should be performed at least annually or whenever major business changes occur. Frequent reviews help update controls and detect new vulnerabilities.

Unusual spending patterns, duplicate payments, and login attempts from unknown locations are common signs. Monitoring these indicators is key to preventing fraud.