Chargeback fraud is a major problem faced by businesses globally as it is constantly increasing and getting worse over time, with e-commerce transactions being a daily occurrence. In 2023, it was estimated that 238 million chargebacks would be seen in the global ecosystem, raising concerns about the issue. This alarming trend highlights the urgent need for businesses to effectively understand and address chargeback fraud.

What are Chargebacks?

Chargebacks are transaction reversals initiated by a customer's bank or credit card company, usually in response to a dispute. Disputes can result from fraud, dissatisfaction with a product or service, or merchant errors. When a chargeback occurs, the disputed amount is refunded to the customer and deducted from the merchant's account. This process not only leads to direct financial losses for businesses but can also result in increased processing fees, damaged reputation, and potential loss of credit card processing privileges. Chargebacks can be exploited by fraudsters and add a layer of complexity to the challenges merchants face.

What is Chargeback Fraud?

Chargeback fraud occurs when a customer falsely disputes a payment from a credit card. These false claims may include claiming that a product was not received, dissatisfaction, or refusing to authorize a transaction that was charged despite being legitimate. Unlike a normal refund, which requires dealing with the seller, a chargeback allows customers to bypass the seller and receive a refund directly from their bank, which then deducts the amount from the seller's account.

How Does Chargeback Fraud Work?

Chargeback fraud cleverly disguises itself as a legitimate transaction dispute, exploiting the protective mechanisms that banks and credit card companies have set up. Here's how the process typically unfolds:

- Initiation: A fraudster, who may be a genuine customer, purchases using their credit card.

- False Claim: After receiving the product or service, the fraudster contacts their bank or credit card issuer, bypassing the merchant, falsely claiming that the transaction was unauthorized or that the item was never received.

- Bank Action: The bank then initiates a chargeback, crediting the fraudster's account and debiting the merchant's account without immediate input.

- Merchant Response: The merchant is notified and must decide whether to contest the chargeback. Contesting involves providing evidence that the transaction was legitimate, which can be resource-intensive and not always successful.

- Resolution: If the merchant does not contest the chargeback or if the contest is unsuccessful, the chargeback remains, and the fraudster retains both the product and the refunded money.

A common variation involves the fraudster complying only superficially with return policies or chargeback conditions. For instance, they might return an item but claim they did not receive a refund or keep the item after receiving a chargeback refund.

Types of Chargeback Fraud

Chargeback fraud comes in several flavors, each with its own challenges for businesses. Here are some of the most common types of chargeback fraud:

Friendly Fraud

Despite its innocuous name, friendly fraud is anything but friendly. It occurs when a customer purchases and receives the product or service and then dishonestly requests a chargeback from their bank, claiming they never authorized the purchase or didn't receive the item. This fraud is particularly frustrating for merchants because it abuses the trust between consumers and sellers.

Criminal Fraud

This type involves outright theft. A fraudster uses stolen credit card information to make unauthorized purchases. When the rightful cardholder notices these transactions, they request a chargeback. Unfortunately, the merchant is left to cover the loss, even though they were unaware that the transaction was fraudulent.

Triangulation Fraud

This sophisticated scam involves the fraudster, the unsuspecting customer, and the legitimate merchant. The fraudster creates a fake online store offering high-demand goods at low prices, collects payment and credit card details, and then uses those details to buy goods from a real store and ship them to the customer. When cardholders see unauthorized charges, they file for a chargeback, and the legitimate merchant suffers the financial hit.

Subscription Fraud

This type occurs when customers claim to have canceled a subscription but continue to use the service, or they might continue being charged due to a clerical error and then initiate a chargeback, claiming they were charged after a cancellation.

Merchant Error

Not all chargebacks stem from malicious intent. Sometimes, they result from honest mistakes by the merchant, such as double billing, shipping the wrong item, or failing to process a return properly. These aren't fraudulent but can lead to chargebacks if not quickly corrected.

How Are Businesses Affected by Chargeback Fraud

Chargeback fraud is a significant financial drain on businesses, affecting them in both direct and indirect ways.

- Financial Costs: For every dollar lost to a chargeback, merchants can end up paying between 1.5 to 2.5 times the disputed amount when accounting for fees, which can range from $20 to $100 per incident. This means that the total cost to the merchant can be as much as 260% of the item's original sale price.

- Lost Inventory: When a chargeback is initiated, the fraudster is often not required to return the product. This results in a double loss for the business – both the revenue from the sale and the physical inventory.

- Increased Monitoring and Compliance Costs: Banks monitor the frequency of chargebacks for each merchant. If a business's chargeback ratio exceeds 1%, it may face additional fees, be placed on a monitoring program, or even be cut off from processing payments altogether. This increases not only operational costs but also compliance risks, as fraudulent chargebacks can be linked to more severe financial crimes like money laundering.

- Operational Disruptions: Implementing and maintaining anti-fraud solutions incurs significant costs. Moreover, every moment spent resolving chargebacks is time that could have been invested in serving genuine customers or growing the business. The operational strain affects various departments, including customer service, finance, and sales.

- Reputational Damage: Excessive chargebacks can lead businesses to be blacklisted by firms or face reluctance from others to engage in business, severely impacting future profit opportunities.

- Long-term Consequences: If chargeback rates become excessive, a merchant might be placed in a high-risk category by credit card networks, leading to hefty fines and higher processing fees. In extreme cases, it could even result in the termination of their merchant account.

Chargeback fraud poses a complex challenge that requires robust management to protect the financial health and operational integrity of businesses. As reported, 90% of firms feel the impact of chargeback abuse, with only a minority effectively managing it. This underscores the need for comprehensive strategies to mitigate these risks and safeguard business interests.

How to Prevent Chargeback Fraud

Chargeback fraud can be particularly challenging because it occurs after a transaction has already been completed. While some companies attempt to address chargeback fraud reactively, the most effective strategies are proactive, focusing on preventing chargebacks from occurring in the first place. Here are several strategies businesses can implement to safeguard against chargeback fraud:

- Implement Robust Credit Card Verification Systems: To prevent criminal fraud-related chargebacks, it's crucial to verify credit card transactions before they are processed. Utilizing identity verification and fraud detection tools, such as the Address Verification System (AVS), helps ensure that credit cards are being used by their rightful owners. Preventing a fraudulent transaction from occurring is far more efficient than dealing with its aftermath.

- Flag Unusual Transactions: Monitoring for unusual purchasing behaviors, such as large or repeated small transactions that could indicate a fraudster's intent to file chargebacks later, is essential. Implementing tools for suspicious activity monitoring and link analysis can help identify and block these transactions before they lead to chargeback fraud.

- Establish Clear Policies and Communications: A significant portion of friendly fraud arises from misunderstandings. Customers might not recognize a charge if the merchant's billing descriptor is unclear. Ensuring that billing descriptions accurately reflect the business's name and the nature of the transaction can reduce confusion. Additionally, having a straightforward and easily accessible return policy can deter customers from resorting to chargebacks as a first option.

- Log Evidence of Transactions: Keeping detailed records of transactions, including sending receipt emails and using package tracking services that require proof of delivery, provides valuable evidence in the event of a dispute. This documentation can prove that a transaction occurred or that a product was delivered as agreed.

- Improve Customer Service: Excellent customer service can significantly reduce chargebacks due to dissatisfaction. By being readily available to address customer concerns and questions, businesses can resolve issues before they escalate into chargebacks.

- Use Robust Fraud-Prevention Tools: Advanced tools like Sanction Scanner use machine learning to analyze transaction data and flag suspicious activities. These tools can detect and prevent potentially fraudulent transactions, reducing the likelihood of chargebacks.

- Manage Chargebacks Effectively: Keeping track of chargeback data and understanding the reasons behind them can help businesses dispute fraudulent or unwarranted chargebacks effectively. Analyzing patterns in chargeback reasons can also provide insights into potential vulnerabilities in the transaction process.

How Can the Sanction Scanner Help

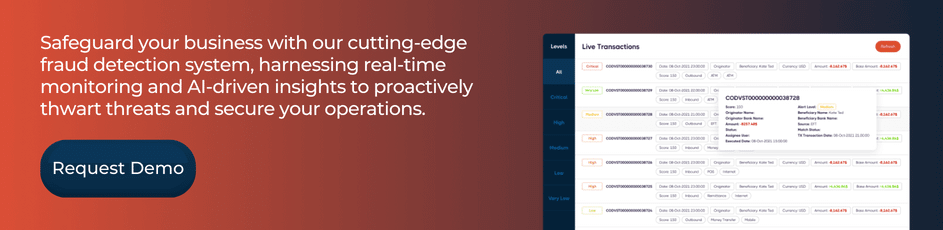

The Sanction Scanner is invaluable in combating chargeback fraud, offering tailored fraud detection capabilities that significantly reduce false positives by up to 96.99%. Its rule-based screening allows businesses to customize detection thresholds and precisely monitor transactions, aligning closely with specific industry needs. The platform's dynamic alert system provides real-time, actionable alerts for high-priority issues, enabling swift and accurate responses.

Additionally, the Sanction Scanner integrates with existing systems via a robust API, ensuring minimal disruption and real-time oversight. Its user-friendly interface makes setting up and managing fraud detection rules straightforward, requiring no coding knowledge. This comprehensive approach sharpens your fraud detection efforts and boosts overall fraud management efficiency. Schedule a demo today to see how the Sanction Scanner can protect your business.